I went to the Small Business Expo held in NYC last week. This end of the company size/age spectrum is not where I spend a lot of my time, but I do start-ups and it was worth the trip to go (and I got a great workout walking cross-town).

I went to the Small Business Expo held in NYC last week. This end of the company size/age spectrum is not where I spend a lot of my time, but I do start-ups and it was worth the trip to go (and I got a great workout walking cross-town).

What I found, by way of vendors was extremely interesting.

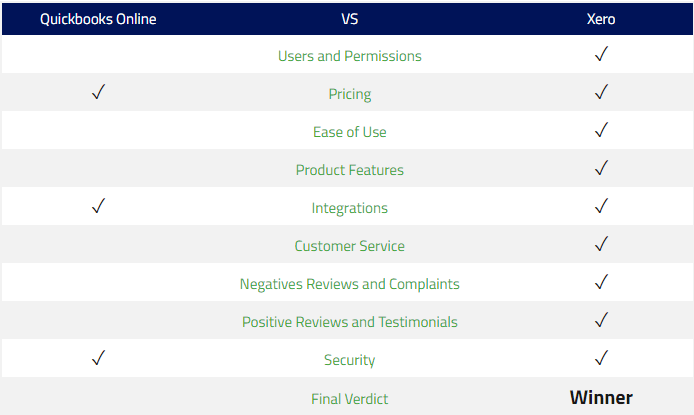

There were no accounting system vendors like Xero or Quickbooks. Strange as this is definitely fertile ground for sales. There was one single bookkeeping service and one non-affiliated CPA. Again, prime sources of new clientele. These three groups provide the basis for financial/tax services to small businesses.

In addition there was a smattering of the larger generic banks and a plethora of funding companies (factors, ABL and others of dubious nature), more about these later.

Lastly, a few franchise brokers attended.

Why small business refuse to get financially well informed

I think it comes down to tunnel vision. If the process does not directly drive revenue, than that is a cost. Expenses are to be avoided at all costs (sorry for the pun and cliché); unless of course that cost can offset a personal cash outlay, (we are speaking T&E, electronics and auto leases). Therefore, whom or what function in a company, especially when your mindset and point of view is so narrow; screams expense. Accounting/Finance of course.

Why hire an accountant who is trained to analyze financial performance, where a bookkeeper will do? Why have little to no internal controls and misplaced trust when it is just easier to delegate without providing proper and timely supervision? Why have a business plan and gauge your success against that plan, because it costs money to track money!

So many small businesses take the cheap way out. Cheap is not inexpensive. Cheap the state of “is not fully understanding the tradeoff” today and the loss of service value versus the increased cost to obtain that same level of value later.

An example could be implementing a system that will only be able to handle your company for 12 months of estimated growth versus spending more now and not have to implement two systems for the next several years. System implementation, whatever that system is, from computers to software, an office floor plan to leasing a copier, is expensive, in both time spent, loss of other opportunities and salaries and consulting fees. One must look past today and see where you think you will be in the mid-term.

The entrepreneurial myopia against finances can have some dire consequences. It causes bad decisions to be made, due to lack of information, and forecasting made by experienced and qualified staff or advisors (who themselves cost money and don’t generate revenues).

The funding companies

I mentioned the fair number of funding companies present at this Expo.

All companies need working capital. Working capital comes from three sources, organic, investors and creditors.

Organic is though sales. As revenue grows so should the contribution margin. So as revenue is growing, hopefully, and if the company has and is following their budget; and at the same time is practicing cost containment, working capital will grow.

When costs are growing faster than sales, not an unexpected event in a start-up, working capital will need to be infused. One can either borrow which means you need to pay it back usually monthly plus interest or let someone buy into the business, and never be obligated to pay it back.

So, you either sell a piece of the business, gain a partner who may or may not have other benefits, synergies or disadvantages (like being intrusive or annoying) or borrow the money and have an entity who is looking for the cash every month, and with lots of penalties if you fail to pay on time.

Funding companies want you to take their money. They in return charge you interest (whether they call it that or not). They also charge you fees for certain services (whether they themselves pay a fee or not for that service). Between interest and service fees, the adjusted APR can get quite steep.

Also, many of these funding houses are predatory; they are not your friend and don’t ever be fooled into thinking that they are. Other funding houses do try to help and do, for a fee, provide services that are beneficial and priced correctly. But remember, they are in business and the concept of business is to make money. Caveat Emptor.

So, I started walking around to all these funding companies. I just wanted to know the answer to one question. What is your APR? If they said it depends on [fill in a factor or issue], I just clarified it as what is your highest APR rate you may charge. Not only is it a simple question, but NYS Banking Laws require full disclosure, so you really need to tell the customer.

The answers were quite astounding. In New York State, which has complicated law structure, at least when it comes to loans finding out what the legal maximum interest rate for a loan can be daunting. One needs to look in two places, one for civil usury and another for criminal usury. The former is found in the banking laws and the latter, the penal code. However, for simplicity sake, for private loans under $2.5M, the criminal usury maximum is 25%.

I was being told rates from 9% to 50%. I was told by one company that they don’t release that information. Another person told me the APR is not important, it is the IRR (what?). One firm stated quite clearly that the broker could make as much as eight (8) points, where another had a placard of a fictitious client saying “I don’t want to sell a piece of my business to obtain working capital, instead I went to xyz”.

Needless to say there were some vendors that were honest and their fees were within the norm for third-tier lending.

Exits and Investments

Lastly, why would these small firms not want to, from the get-go, set themselves up so if they had an opportunity for an exit or a major investor buying in, that they be ready? It makes no sense.

However, does it? In some respects, many small entrepreneurs have a million dollar idea and just want to run with that idea. They are going to make so much money, that it does not matter. That is the Facebook or LinkedIn folklore, but both of these companies had scores of professionals, both on staff and as consultants, making sure everything was just right for the IPO or sale.

I guess the small businesspeople just miss that paragraph.

Counsel

If you are a small firm (even a larger than small firm) it behooves management to understand and embrace the financial-accounting aspect of the business.

Get professionals on you team, the right CFO and/or Controller. The CPA/Audit firm and a good General Counsel that has experience (real experience) in you market. Too many times people ask favors of friends who are lawyers and they get fuzzy answers that they rely on. Just because you do corporate law, the laws concerning basket weaving may be different and that difference could mean winning or losing both in and out of court.

Released: April 3rd, 2017

Released: April 3rd, 2017

This was the title of a series of posts on the CFO centric website Proformative.com. SaaS, which is Software as a Service is the newest tweak to the computer world and Internet.

This was the title of a series of posts on the CFO centric website Proformative.com. SaaS, which is Software as a Service is the newest tweak to the computer world and Internet.